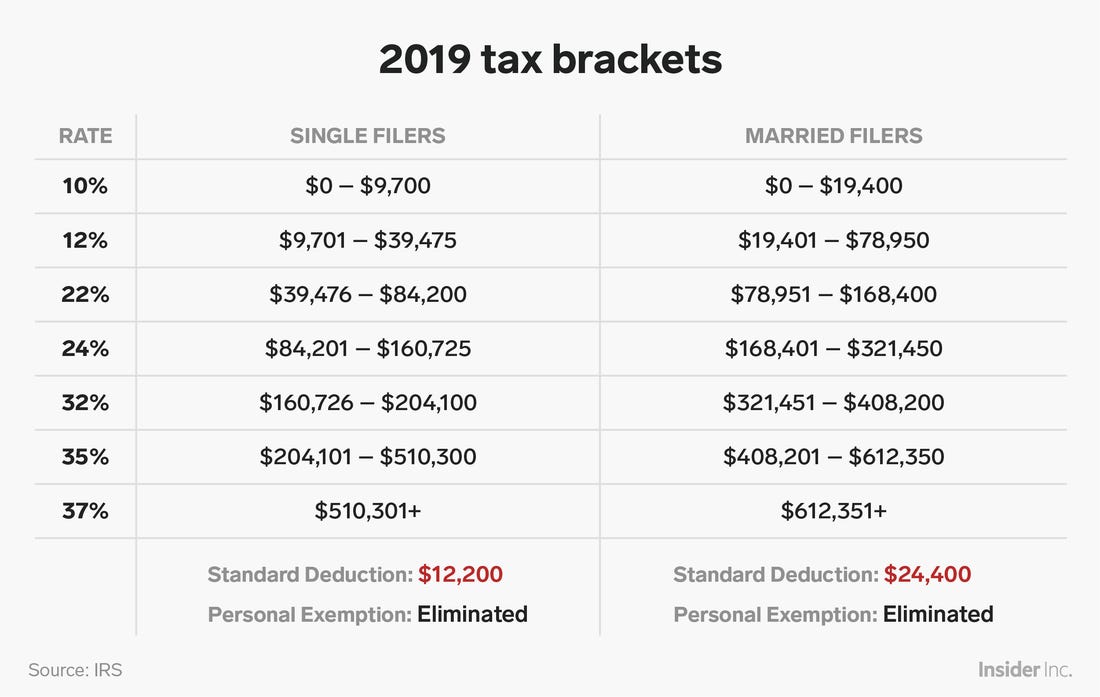

I now know there are a variety of methods and strategies to invest. That is part of what has created analysis paralysis in so many educators in schools. In addition to IRAs, which everyone has access to, educators (and other state employees) have access to two special options that sound like just a bunch of arbitrary numbers - the 457 and the 403b. Great, more options, right? But. these are tax advantaged accounts, similar to the more commonly heard of 401k. If you have a part of your salary deducted and immediately placed into these accounts, that PART of your salary can be non-taxable (for now)! I had to look into tax rates to try to get a better understanding of this. so let me give you the summarized version. Tax brackets show you the tax rate you will pay on each portion of your income.  I'm married, so I'll use the "married" example. So, as a married person (filing jointly), If we earned $19,000, the tax rate of 10% would be applied to our entire income. But, if we together made $50,000, what would happen? Income from $0-19,400 would be taxed at 10%. Income from $19,401 to our $50,000 would then be taxed at 12%.

What makes tax advantaged accounts, like the 401k (at most companies), 403b, 457, cool is that money is legally "hidden" as far as taxes are concerned. If we earned $50,000, but put $30,600 into tax advantaged accounts, it will look like we only earned $19,400! And all that money is still ours, but saved for our future selves. Obviously, you'd have to budget and figure how much you need to live on now and how much you'll need to live on later to see what would work best in your situation. Besides being tax advantaged, I can tell you that a 403b is a nonprofit version of a 401k. It grows tax free, but you will pay taxes whenever you do eventually pull money out. There are limits to how much you can put in to this kind of account. In 2020, the max you can put in is $19,500. If you take money out of these accounts before retirement age though, you'd incur extremely high fees. MOST 403b accounts are tricky and expensive! They charge hidden, very expensive fees. They also employ very friendly salespeople to lure you in with free food to your own teacher's lounge. So, in general, if you are using am annuity product or anything with the idea of "insurance" in the name - IT'S A TRICK - RUN! There are a handful of FANTASTIC, low fee, self directed options though that if you can find, you should get involved with ASAP. In my research so far, it looks like Vanguard, Fidelity, T. Rowe, and Aspire are GREAT options. Definitely do a bit of research to figure out what you're most comfortable with. A great place to research the options is 403bwise.org and 403bcompare.com. 457s are unique to state employees and generally are very similar to 403bs. Often, states have their own 457/deferred compensation plans. They also have that $19,500 limit, BUT AS AN EDUCATOR, YOU CAN FILL BOTH the 457 and the 403b, granting you $39,000 in tax advantaged (hidden) money! 457s are unique also because you may be able to access this money BEFORE retirement age IF you leave your district. This means you could accept a job at a new district, start putting money into THEIR 457 account, and start withdrawing money from the previous district's account! Certain people (see the Millionaire Educator) have made mixed their financial planning with a little game theory to spin this money in magical ways. You can read up on his journey here. In trying to learn more about these things, I've reached out to several people in the field who have agreed to speak to me. I will follow up in August with information from these zoom sessions.

0 Comments

Leave a Reply. |

AuthorJoin me, the Penny Pinching Pathologist, on a journey of financial discovery. How can we educate ourselves on financial fluency for school workers and other governmental employees? Archives

August 2020

Categories |

RSS Feed

RSS Feed